This article, explores the bank reconciliation definition, process, reasons to prepare the statement, examples, importance, and FAQs.

What is a Bank Reconciliation Statement?

A bank reconciliation statement (BRS) is a statement of the document which measures and compares the cash balance (respective company’s balance sheet) to the corresponding amount on the respective bank statement. The main purpose to compare those accounts, i.e., to reconcile those accounts is to, identify whether there is any need for accounting changes.

Bank reconciliation will be measured and closed at the regular interval of time. It helps the company or an organization to make sure that all their cash records are correct. Thus, it is easy for a company to detect in case of any cash manipulation or even fraud.

The BRS outlines every activity affecting a bank account such as deposits, withdrawals, and so on, for a particular period of time. Nowadays there are bank reconciliation artificial intelligence tools available which can do most of the reconciliation work

In simple words, a bank reconciliation statement (BRS) is a document that will be prepared for reconciling the dissimilarities between the balance as per the passbook given respective date and cash books bank column.

Bank Reconciliation process

Here is the complete procedure for bank reconciliation. The steps are as follows.

Get the bank records

The first step is you require access to the list of your business transactions. So that you can proceed to reconcile. It can be done in 2 different ways.

- Either you can get these data with the help of online banking as a bank statement.

- Or through the accounting software. You can authorize your bank to transfer data through your accounting software.

Collect all your business records

In addition to having access to the list of transactions, you should have access to the respective company’s books or ledger. This record of information is maintained on accounting software or in the form of a spreadsheet or logbook.

The starting point

The starting point of your bank reconciliation process depends on your last balanced book date. In case of feeling confused with the starting point, try to mention when your books matched the bank account balance and have a start at that point.

Go through all your company’s deposits and withdrawals of the bank

Have a clear picture and analysis that all your bank deposits and withdrawals are exactly accounted with the bank statement perspective. In case, if you found any item that is not added or missing, make sure to add it to the bank statement.

Analyze the book’s income and expense

Check your books corresponding to bank statements, and have a clear record that all your business transactions are accounted for accurately. If you found any mismatch in the record, then analyze why it is mismatched. And make it in the right way.

Adjustments made on bank statements

The business records cannot be accurate and perfect all the time. There might be a chance of error and mismatch between the bank statement and your company’s transactions. Due to deposits that are still in transit, bank errors, or outstanding checks, it might happen. Rectify the errors and proceed with the accurate bank reconciliation process.

End balance comparison

When all issues are rectified and your business records get matched, make sure that the end balance is the same at last to complete the bank reconciliation process. If the records are clear and matched, the process is completed successfully. If it doesn’t then you need to repeat the above process.

Why Prepare a Bank Reconciliation statement?

There is no compulsion or mandatory to prepare a bank reconciliation statement. Additionally, there is no proper fixed date to prepare the bank reconciliation statement.

The bank reconciliation statement is prepared as per the company/s periodical basis. It just checks, whether all the bank correlated transactions are recorded correctly in the cashbook’s bank column and additionally by the respective bank in their book.

Thus, the bank reconciliation statement helps you

- In tracking errors on the recorded transactions.

- Measuring the accurate bank balance as on the mentioned date.

Example of Bank Reconciliation:

Let’s consider some examples for understanding bank reconciliation.

Bank Reconciliation Example: 1

Let’s consider a company XYZ. XYZ has a balance as per the passbook of $2000 as of 30th April 2021. It has a balance as per the cash book as of 30th April 2021 of $2150. Additional details are given below.

- A cheque worth $500 was deposited. But it was not collected by the bank.

- Recorded – $100 as bank charge in the passbook. But it is not recorded on the cash book.

- $300 cheque worth has been processed and issued. But it is not presented for payment.

- Recorded – $150 as bank interest in a passbook. But it is not recorded on the cash book.

Solution:

Particulars | Amount | Amount |

PassBook Balance | - | $2000 |

Add: Deposited, but was not collected check | $500 | - |

The charges of the bank not recorded on the cash book | $100 | $600 |

Less: Issued check not presented for the payment | $300 | - |

Received bank interest. But not recorded in cash book | $150 | ($450) |

Cash Book Balance | - | $2150 |

Bank Reconciliation Example: 2

Let’s consider a company ABC. ABC has a balance in a passbook for $15,000 as of December 31st, 2021. The other details are below.

- There are 3 cheques deposited on December 30th, 2020 in the bank, worth $1000, $2500, and $3000. But the bank statement is recorded on 2021st of January.

- A cheque was issued on December 31st, 2020, worth $1000. But it is not mentioned or presented for payment.

- In a bank account, it was credited as a dividend of $1,500 on stocks. But the point is not recorded on the cash book.

- A customer made a direct deposit of $500 in the bank account. But this is also not recorded on the cash book.

- The charges of the bank entered only on bank passbook, worth $200.

- As per the Cash Book balance, December 31st, 2020 is $18700

Particulars | Amount | Amount |

Passbook Balance | - | $15000 |

Add: Deposited cheques (But which is not collected by the bank) ($1000 + $2500 + $3000) | $6500 | - |

The charges of the bank entered only on bank passbook | $200 | $6700 |

Less: Issued cheque not presented on payment | $1000 | - |

Bank collected dividends | $1500 | - |

Direct deposit (not recorded in cash book) | $500 | ($3000) |

Cashbook Balance | - | $18700 |

Bank Reconciliation Example: 3

Company ABC has a difference in balance as per the bank statement and Cash Book on April 30th, 2020. Now you are requested to make a Bank reconciliation statement on the date with the below information.

- Balance as per Bank Statement is $9000 on April 30th 2020. The Cash Book balance is $900.

- A cheque of $1500 and $1000 issued as of April 30th, 2020. But it is not cleared yet.

- An insurance premium of $500 paid by the bank, not recorded yet in the cash book.

- An outing cheque was recorded twice in the cash book, worth $3000. It is recorded perfectly on a bank statement.

- $500 cheque worth payment recorded in passbook for twice.

- Dividends received $600. It is recorded on the bank statement and not recorded on the cash book.

- A cheque worth $900 was deposited on April 28th, 2020. But was not collected.

- Bank charges of $200 debited only in Bank PassBook.

Solution:

Particulars | Amount | Amount |

Passbook Balance | - | $9000 |

Add: Bank's - Paid premium insurance | $500 | - |

Deposite cheque (But not collecte yet) | $900 | - |

In passbook, cheque recorded for twice | $500 | - |

Charges debited on passbook but not cashbook on bank | $200 | $2100 |

Less: Issued cheque (not presented for payment- $1500 $1000) | $2500 | - |

Cheque recorded in cashbook for twice | $3000 | - |

Received dividends recorded on bank statement only | $600 | ($6100) |

Cash Book Balance | - | $800 |

Download your Bank Reconciliation Excel Template

Importance of Bank Reconciliation

It is not mandatory to prepare a bank reconciliation statement. But it helps you to detect cases of any cash manipulation or even fraud.

Below points are some of the importance of bank reconciliation:

- First and foremost is to watch out for errors. It might happen in the cash book in connection with bank transactions. If you want to trace those errors or mistakes that could be made simple and easy with the help of this statement.

- When you make this process regularly with good research, it prevents you from fraud.

- This statement is not only important to the internal auditors but also to the management. Management must take corrective action against accounting staff after receiving comments from internal auditors.

- It is the process of comparing bank withdrawals, deposits, and credits against the Cash Book to check that they agree with each other. It helps you in cash book updation by discovering some not recorded entries yet.

- You can maintain a healthy relationship between the banks and their respective customers when you maintain a healthy reconcile book. Sometimes, bank reconciliation of your books is critical to maintain the financial integrity of your business

- With the help of a bank reconciliation statement, it is easy to maintain all your up-to-date records. It helps you to manage and avoid unnecessary delays in both payment and collections.

Bank Reconciliation Statement FAQ’s

Who prepares the bank reconciliation statement?

In general, It is prepared by your business accountant. In some of the cases, it is also prepared by your bookkeepers. The purpose of preparing the statement is to compare both your business and bank record. It is prepared per month, whenever the bank statement tent to arrive. This statement is prepared by using all your previous day’s transactions.

Which two books are compared for the preparation of bank reconciliation statements?

The cash book and the passbook are the two books compared for the preparation of these statements.

What are the rules for preparing this statement?

To know anything perfect, study and follow their respective rules. Likewise, to make an accurate statement, follow the below-mentioned rules.

- The debit in the cashbook must be similar to the credit in the passbook.

- If it is a credit balance in the cash book, it is an unfavorable balance, and if the debit balance is in the cash book, it is a favorable balance.

- Any of the debit balance in the cash book is directed as the deposits of the business activity.

- Cheques are issued but, in case of unavailability, it is adjusted in the cashbook.

How do you record errors in a bank reconciliation?

The main errors to record are – dates mismatch and amount mismatch. In case of an error in the date mismatch, compare your bank statement date with your account book date and finally, you can record the error in it.

In the case of an amount mismatch, do the similar by comparing your account book with the bank statement and record the error.

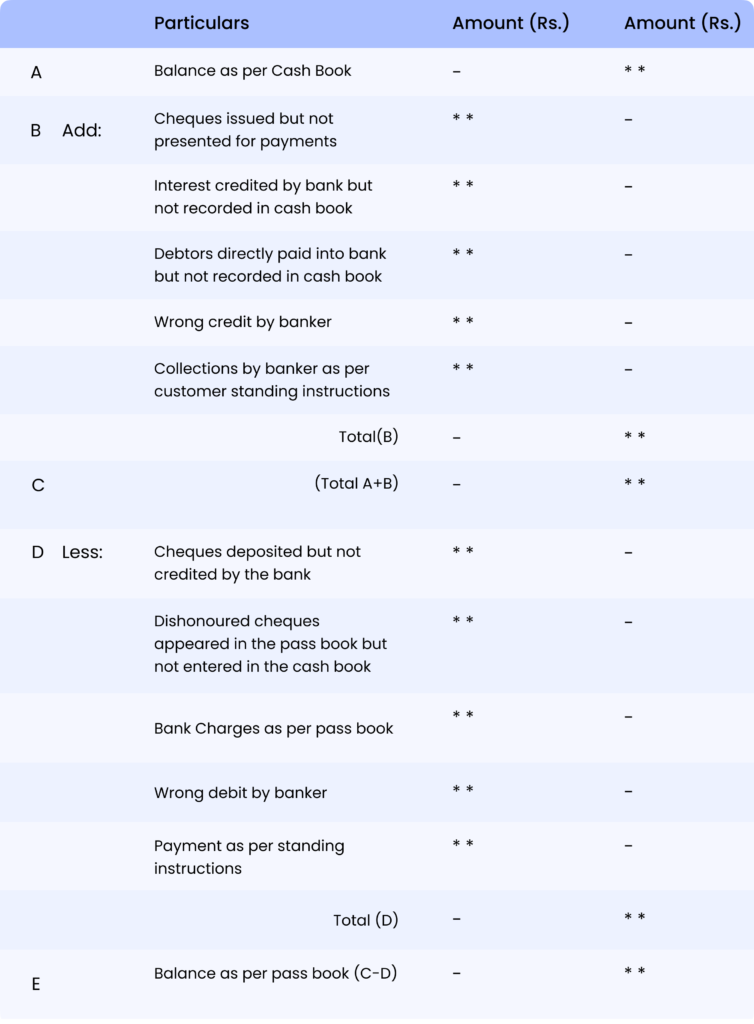

What is the bank reconciliation statement format?